Market Outlook

March 15, 2018

Market Cues

Domestic Indices

Chg (%)

(Pts)

(Cl ose)

Indian markets are likely to open negative tracking global indices and SGX Nifty.

BSE Sensex

(0.2)

(61)

33,857

U.S. stocks fell sharply during the last trading session, accelerating to the downside

Nifty

0.1

5

10,427

after a relatively upbeat start to the session. The Dow Jones slipped to 1.0% to close

Mid Cap

1.0

161

16,269

at 24,758. The NASDAQ dropped down by 0.2% to close at 7,497.

Small Cap

1.1

199

17,602

U.K. stocks finished down slightly the last trading session, tracking losses in the U.S.

Bankex

0.4

121

27,905

that came as trade-war fears helped send industrial shares lower. The FTSE 100 was

down by 0.1% to end at 7,133.

Global Indices

Chg (%)

(Pts)

(Cl ose)

On domestic front, Indian shares opened lower as trade tensions between the U.S.

Dow Jones

(1.0)

(249)

24,758

and China intensified and Punjab National Bank said it has uncovered additional

Nasdaq

(0.2)

(14)

7,497

exposure of about Rs 942cr to Gitanjali Group under consortium lending. The BSE

FTSE

(0.1)

(6)

7,133

Sensex ended down by 0.2% at 33,857.

Nikkei

(0.6)

(128)

21,649

News Analysis

Hang Seng

(0.1)

(22)

31,413

World Bank projects 7.3% growth for India in FY19 and 7.5% in FY20

Shanghai Com

(0.1)

(4)

3,288

Detailed analysis on Pg2

A dvances / Declines

BSE

NSE

Investor’s Ready Reckoner

Advances

1,279

868

Key Domestic & Global Indicators

Declines

1,423

896

Stock Watch: Latest investment recommendations on 150+ stocks

Unchanged

155

76

Refer Pg5 onwards

Top Picks

Volumes (` Cr)

C MP

Target

U psi de

C ompany

Sector

R ating

BSE

3,388

(`)

(`)

(%)

Alkem Laboratories

Pharmaceuticals Accumulate

2,197

2,441

11.1

NSE

27,629

Blue Star

Capital Goods Accumulate

797

867

8.8

Dewan Housi ng Finance

Financials

Buy

522

720

38.0

Net Inflows (` Cr)

Ne t

Mtd

Ytd

Karur Vysya Bank

Financials

Buy

102

160

57.5

FII

4,935

8,340

8,833

KEI Industrie s

Capital Goods

Buy

372

436

17.3

*MFs

(273)

(455)

24,750

More Top Picks on Pg4

Key Upcoming Events

Top Gainers

Price (`)

Chg (%)

Previous

C onsensus

D ate

Region

Event Description

Reading

Expectations

IDBI

74

10.2

Mar 15

India

Imports YoY%

26.10

JPASSOCIAT

16

9.4

Mar 15

US

Initial Jobless claims

231.00

227.50

JAICORPLTD

141

7.4

Mar 15

India

Exports YoY%

9.10

DISHTV

71

7.2

Mar 16

US

Housi ng Starts

1,326.00

1,290.00

Mar 16

Euro Zone

Euro-Zone CPI (YoY)

1.20

1.20

ORIENTBANK

101

6.1

More Events on Pg7

Top Losers

Price (`)

Chg (%)

IIFL

814

(4.3)

GDL

205

(3.9)

DEEPAKFERT

323

(3.8)

IBVENTURES

260

(3.8)

BBTC

1,293

(3.7)

As on March 14, 2018

Market Outlook

March 15, 2018

News Analysis

World Bank projects 7.3% growth for India in FY19 and 7.5% in FY20

The World Bank projected India's GDP growth at 7.3 per cent for the next financial

year and accelerates further to 7.5 per cent in 2019-20. The report, however,

observed that a growth of over 8 per cent will require "continued reform and a

widening of their scope" aimed at resolving issues related to credit and investment,

and enhancing competitiveness of exports.

"The Indian economy is likely to recover from the impact of demonetization and

the GST, and growth should revert slowly to a level consistent with its proximate

factors - that is, to about 7.5 per cent a year". The World Bank report further said

that accelerating the growth rate will also require continued integration into global

economy.

Economic and Political News

Government approves Rs 64.41bn road projects under SARDP programme

for Nagaland

Hindustan Unilever's GST benefit deposit offer to Government touches Rs

1.55bn

Government released Rs 125bn to Andhra as special assistance

Corporate News

Tata Teleservices plans to close CDMA service in Delhi from March 19

ITI Ltd to have Rs 100-bn order book by March-end

Wipro to divest hosted data centre services business to Ensono for $405mn

Strides Shasun gets US FDA approval for HIV treatment drug Efavirenz

Market Outlook

March 15, 2018

Top Picks

Market Cap

C MP

Target

Upside

C ompany

R ationale

(` Cr)

(`)

(`)

(%)

Strong growth in domestic business due to its

leadership in acute therapeutic segment. Alkem

Alkem Laboratories

26,270

2,193

2,441

11.1

expects to launch more products in USA, which bodes

for its international business.

Favorable outlook for the AC industry to augur well for

Cooling products busine ss which is out pacing the

Blue Star

7,591

797

867

9.6

market growth. EMPPAC division's profitability to

improve once operating environment turns around.

With a focus on the low and medium income (LMI)

consumer segment, the company has increased its

Dewan Housi ng Finance

16,189

521

720

39.5

presence in tier-II & III cities where the growth

opportunity i s immense.

Well capitalized with CAR of

18.1% which give s

sufficient room to grow asset base. Faster resolution of

ICICI Bank

195,338

306

416

36.6

NPA would reduce provision cost, which would help to

report better ROE.

High order book execution in EPC segment, rising B2C

KEI Industrie s

2,896

371

436

18.0

sales and higher exports to boost the revenues and

profitability

Expected to benefit from the lower capex requirement

Music Broadcast Limited

2,166

378

475

25.1

and 15 ye ar long radio broadcast licensing.

Massive capacity expansion along with rail advantage

Navkar Corporation

2,389

157

265

67.0

at ICD as well CFS augur well for the company

Strong brands and distribution network would boost

Siyaram Silk Mills

2,961

628

851

34.7

growth going ahead. Stock currently trade s at an

inexpensive valuation.

Market leadership in Hi ndi news genre and no.

2

viewership ranking in English news genre, exit from the

TV Today Network

2,718

535

508

11.5

radio business, and anticipate d growth i n ad spends

by corporate to benefit the stock.

After GST, the company is expected to see higher

volume s along with improving product mix. The

Maruti

2,64,426

8,839

10,619

21.3

Gujarat plant will also e nable higher operating

leverage which will be margin accretive.

We expect loan book to grow at 24.3% over next two

GIC Housing

2,139

396

655

64.9

year; change in borrowing mix will help in NIM

improve ment

We expect CPIL to report net Revenue/PAT CAGR of

~17%/ 16% over FY2017-20E mainly due to he althy

Century Plyboards

7,253

322

400

22.5

growth in plywood & lamination busi ness, forayed into

MDF & Particle boards on back of strong brand &

distribution network.

We expect sales/PAT to grow at 13.5%/20% over next

LT Foods

2,765

86

128

48.1

two years on the back of strong distribution network &

addition of new products in portfolio.

Third largest brand pl ay in luggage segment Increased

product offerings and improving distri bution network is

Safari Industries

1,181

531

650

22.4

leading to strong growth in business. Likely to post

robust growth for next 3-4 years

We expect HSIL to report PAT CAGR of ~15% over

FY2017-20E owing to better improve ment in operating

HSIL Ltd

2,969

405

510

24.2

margin due price hike in container glass segment,

turnaround in consumer business.

We expect financialisation of savings and increasing

Aditya Birla Capital

33728

151

218

41.5

penetration in Insurance & Mutual fund would ensure

steady growth.

Source: Company, Angel Research

Market Outlook

March 15, 2018

Fundamental Call

Market Cap

C MP

Target

Upside

C ompany

R ationale

(` Cr)

(`)

(`)

(%)

CCL is likely to maintain the strong growth trajectory

CCL Products

3,882

292

360

23.4

over FY18-20 backed by capacity expansi on and new

geographical foray

We forecast Nilkamal to report top-line CAGR of ~9%

to `2,635cr over FY17-20E on the back of healthy

Nilkamal

2,510

1,682

2,178

29.5

demand growth in pl astic division. On the bottom -line

front, we estimate ~10% CAGR to `162cr owing to

improve ment in volumes.

We expect sales/PAT to grow at 9%/ 14% over next two

years on the back of healthy demand growth in

Shreyans Industries

191

138

247

79.2

printing. Further, China had banned maki ng paper

from waste pulp which would benefit Indian paper

companie s.

The prism has diversified exposure in the different

segment such as Cement, Tile & ready mix concrete.

Prism Cement

5,932

118

160

35.8

Thus we believe, PCL is in the right place to capture

ongoing government spendi ng on affordable housing

and infrastructure projects.

Elantas Beck India is the Indian market leader in liquid

insulation segment use d in electrical equipments like

Elantas Beck India Ltd

1,614

2,036

2,500

22.8

motors, transformers etc. It derives demand from

several industries which are expected to register 10%+

CAGR in demand in the coming years.

RPL to report healthy top-line CAGR of ~13% over

FY17-20E on the back of healthy de mand in printing &

Ruchira Papers Ltd.

378

169

244

44.6

writing paper segments. On the bottom-line front, we

estimate ~16% CAGR over FY17-20E owing to strong

improve ment in operating performance.

Greenply Industries Ltd (GIL) manufactures plywood &

allied products and medium density fibreboards

(MDF). GIL to report net reve nue CAGR of ~14% to

Greenply Industries

3,998

326

395

21.2

~`2,478cr over F Y2017-20E mainly due to healthy

growth in plywood & lamination busine ss on the back

of strong brand and di stribution network

Source: Company, Angel Research

Market Outlook

March 15, 2018

Key Upcoming Events

Global economic events release calendar

Bl oomberg Data

D ate

Time

C ountry

Event Description

Unit

Period

L ast Reporte d

E stimate d

Mar 15, 2018

12: 00 PM India

Monthly Wholesale Prices YoY%

% Change

Feb

2.84

2.50

6:00 PM US

Initial Jobless claims

Thousands

Mar 10

231.00

227.50

US

Producer Price Index (mom)

% Change

Feb

0.70

India

Imports YoY%

% Change

Feb

26.10

6:45 PM US

Industrial Production

%

Feb

(0.05)

0.40

Mar 16, 2018

India

Exports YoY%

% Change

Feb

9.10

3:30 PM Euro Zone

Euro-Zone CPI (YoY)

%

Feb F

1.20

1.20

6:00 PM US

Housi ng Starts

Thousands

Feb

1,326.00

1,290.00

6:00 PM US

Building permits

Thousands

Feb

1,377.00

1,320.00

Mar 20, 2018

8:30 PM Euro Zone

Euro-Zone Consumer Confidence

Value

Mar A

0.10

3:00 PM UK

CPI (YoY)

% Change

Feb

3.00

Mar 21, 2018

7:30 PM US

Existing home sales

Million

Feb

5.38

5.42

3:00 PM UK

Joble ss claims change

% Change

Feb

(7.20)

11: 30 PM US

FOMC rate decision

%

Mar 21

1.50

1.75

Mar 22, 2018

2:00 PM Germany

PMI Services

Value

Mar P

55.30

2:00 PM Germany

PMI Manufacturing

Value

Mar P

60.60

7:30 PM US

New home sales

Thousands

Feb

593.00

617.50

Mar 23, 2018

5:30 PM UK

BOE Announce s rate s

% Ratio

Mar 22

0.50

Mar 27, 2018

7:30 PM US

Consumer Confidence

S.A./ 1985=100

Mar

130.80

Mar 28, 2018

6:00 PM US

GDP Qoq (Annualise d)

% Change

4Q T

2.50

Mar 29, 2018

1:25 PM Germany

Unempl oyment change (000's)

Thousands

Mar

(22.00)

2:00 PM UK

GDP (YoY)

% Change

4Q F

1.40

Mar 31, 2018

6:30 AM China

PMI Manufacturing

Value

Mar

50.30

Apr 03, 2018

2:00 PM UK

PMI Manufacturing

Value

Mar

55.20

Source: Bloomberg, Angel Research

Market Outlook

March 15, 2018

Macro watch

Exhibit 1: Quarterly GDP trends

Exhibit 2: IIP trends

(%)

(%)

10.0

10.0

9.1

8.8

9.0

8.0

8.1

8.0

7.1

7.6

7.6

8.0

7.3

7.2

7.2

6.8

6.0

4.8

7.0

6.5

4.4

6.1

4.1

5.7

4.0

3.2

2.9

6.0

2.0

5.0

2.0

1.2

1.0

4.0

-

3.0

(0.3)

(2.0)

Source: CSO, Angel Research

Source: MOSPI, Angel Research

Exhibit 3: Monthly CPI inflation trends

Exhibit 4: Manufacturing and services PMI

56.0

Mfg. PMI

Services PMI

(%)

6.0

54.0

5.2

5.1

4.9

52.0

5.0

3.9

50.0

3.7

3.6

4.0

3.3

3.3

3.0

48.0

3.0

2.4

2.2

46.0

2.0

1.5

44.0

1.0

42.0

40.0

-

Source: Market, Angel Research; Note: Level above 50 indicates expansion

Source: MOSPI, Angel Research

Exhibit 5: Exports and imports growth trends

Exhibit 6: Key policy rates

(%)

Exports yoy growth

Imports yoy growth

(%)

Repo rate

Reverse Repo rate

CRR

60.0

6.50

50.0

6.00

40.0

5.50

30.0

5.00

20.0

4.50

10.0

4.00

0.0

3.50

(10.0)

3.00

Source: Bloomberg, Angel Research

Source: RBI, Angel Research

Market Outlook

March 15, 2018

Global watch

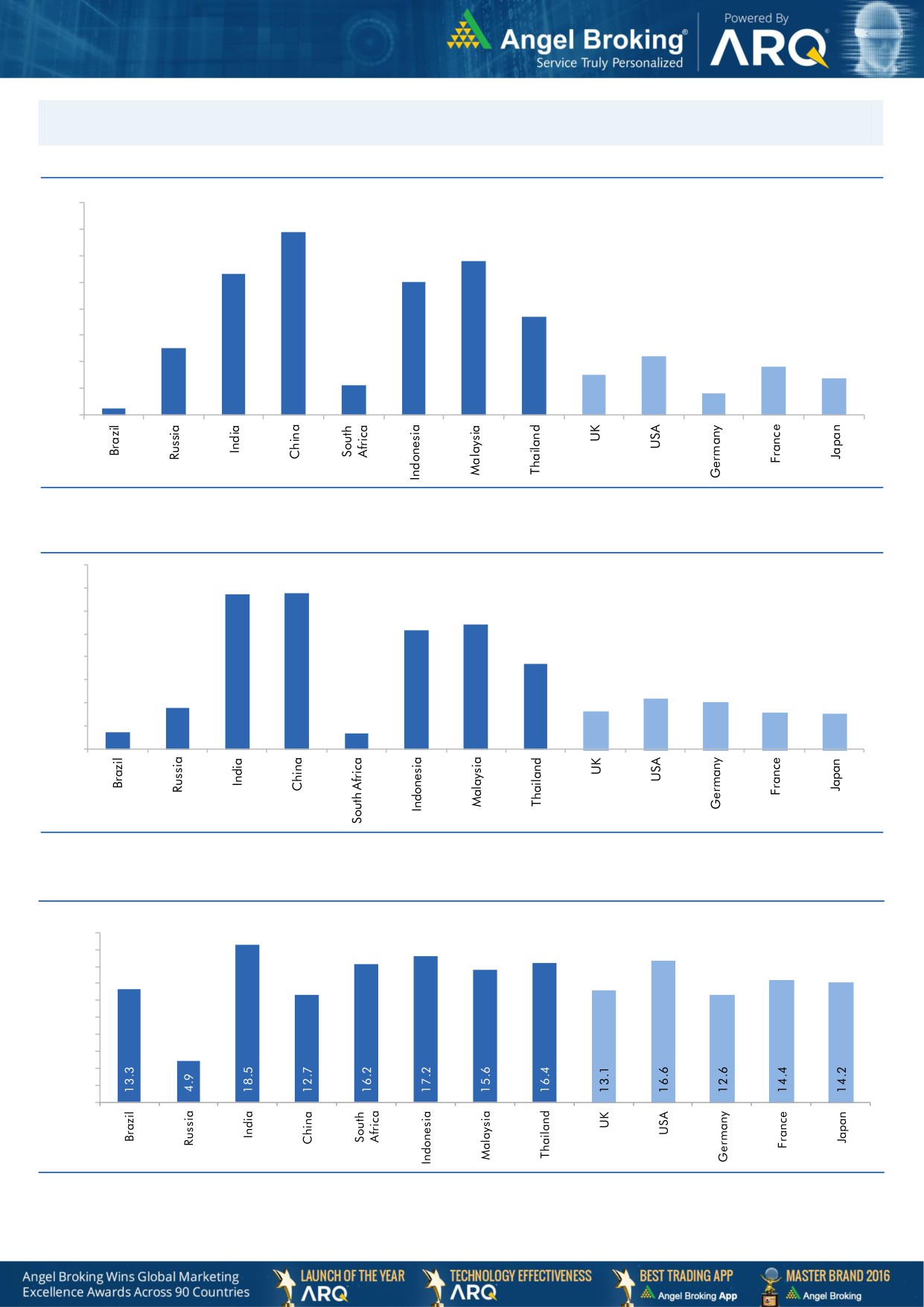

Exhibit 1: Latest quarterly GDP Growth (%, yoy) across select developing and developed countries

(%)

8.0

6.9

7.0

5.8

6.0

5.3

5.0

5.0

1.1

3.7

4.0

2.5

3.0

2.2

1.8

2.0

1.5

1.4

0.8

1.0

0.3

-

Source: Bloomberg, Angel Research

Exhibit 2: 2017 GDP Growth projection by IMF (%, yoy) across select developing and developed countries

(%)

6.7

6.8

7.0

6.0

5.4

5.2

5.0

3.7

4.0

3.0

1.8

2.2

2.0

1.7

1.6

2.0

0.7

1.5

0.7

1.0

-

Source: IMF, Angel Research

Exhibit 3: One year forward P-E ratio across select developing and developed countries

(x)

20.0

18.0

16.0

14.0

12.0

10.0

8.0

6.0

4.0

2.0

-

Source: IMF, Angel Research

Market Outlook

March 15, 2018

Exhibit 4: Relative performance of indices across globe

Returns (%)

C ountry

Name of index

Closing price

1M

3M

1YR

Brazil

Bovespa

86,051

5.5

17.4

30.9

Russia

Micex

2,275

2.2

8.2

13.7

India

Nifty

10,411

(1.6)

1.4

16.6

China

Shanghai Composite

3,291

(2.5)

0.4

1.4

South Africa

Top 40

51,789

4.5

0.2

15.5

Mexico

Mexbol

48,156

0.7

1.2

2.3

Indonesia

LQ45

1,051

(5.1)

2.2

16.6

Malaysia

KLCI

1,857

2.0

8.0

7.5

Thailand

SET 50

1,195

3.5

8.6

22.5

USA

Dow Jones

24,758

2.3

1.8

18.2

UK

FTSE

7,133

(0.6)

(4.3)

(3.8)

Japan

Nikkei

21,777

1.8

(3.2)

12.6

Germany

DAX

12,238

(0.4)

(6.8)

1.9

France

CAC

5,233

1.8

(2.8)

4.4

Source: Bloomberg, Angel Research p68in4